ABLE Accounts and the Household Economic Response to Asset-Test Relief

Asset tests in means-tested transfer programs impose implicit marginal taxes on saving that can exceed one million percent. The 2014 Achieving a Better Life Experience (ABLE) Act relaxes an asset test on the asset margin alone, raising the effective limit for adults with pre-age-26 disability onset from $2,000 to $102,000. Using the staggered state rollout between 2016 and 2026 across three panels, I find asset-test relief raises disposable income for adults with disabilities by 1.49 percent and by $1.59 billion aggregate annually.

Key results

per person, per year

income gain

adults with disabilities

adults with disabilities

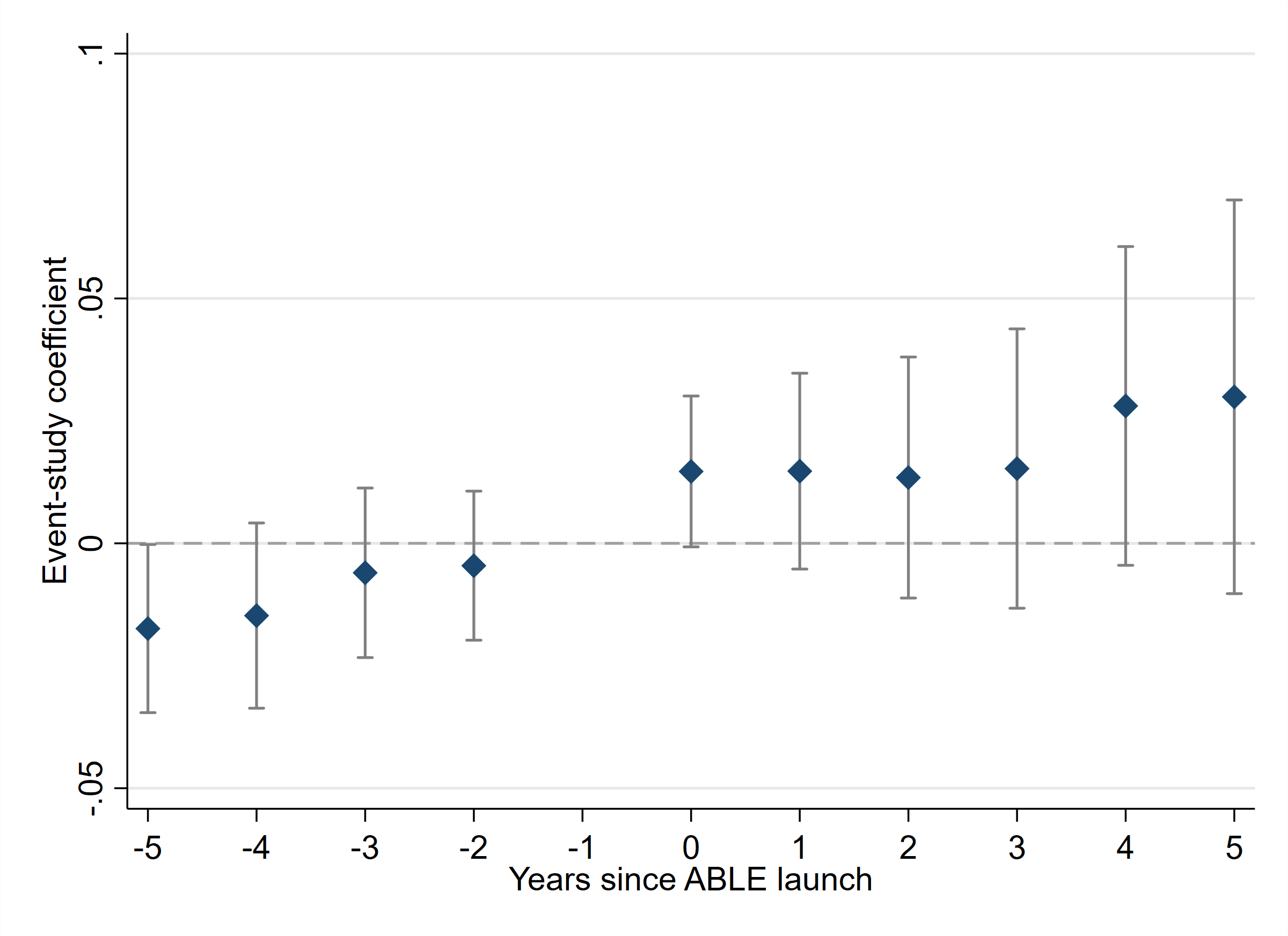

Figure 1: Event study of disposable income around state ABLE program launch

Pre-trends between launcher and control states are statistically indistinguishable from zero. Disposable income for adults with disabilities begins rising in year 1 and grows steadily over the first five years of program availability.

Asset-test relief works.

The ABLE Act raises the effective SSI asset limit for adults with pre-age-26 disability onset from $2,000 to $102,000 without altering income limits, benefit levels, or work incentives. States rolled out programs in a staggered sequence between 2016 and 2026, providing a clean natural experiment.

Impact grows with time in program.

Disposable income rises 1.49 percent, or $321 per person per year, and aggregate disposable income rises $1.59 billion annually. Employment rises 0.67 pp, labor force participation 0.82 pp, log wage income 7.70 percent.

Young adults drive the response.

An age-eligibility quadruple difference concentrates effects among young adults who satisfy the pre-age-26 onset rule automatically. In that group, employment rises 1.84 pp, labor force participation 1.15 pp, and log wage income 22.47 percent.

ABLE and Medicaid expansion substitute.

Effects concentrate in states that did not expand Medicaid under the Affordable Care Act, suggesting the two policies substitute on the income margin.

The 2026 Age Adjustment Act scales impact.

Raising the age-of-onset threshold from 26 to 46 extends eligibility to roughly six million additional adults, including approximately one million veterans, and will scale the aggregate response above the $1.59 billion baseline.

Preliminary state take-up over time

Take-up is uneven. Twenty-nine states publish quarterly assets-under-management figures through Ascensus National ABLE Alliance reports, Vestwell reports, and state Treasurer publications, giving a longitudinal picture from 2016 Q2 through 2026 Q2. Nine states also publish account counts. Take-up scales fastest in first-mover states (Ohio, Tennessee, Nebraska, Virginia). Data are scraped from state Treasurer, Ascensus, and Vestwell public reports on July 13, 2026, and are preliminary.

Assets under management ($M) by state, over time

Assets per resident, by state, over time

Accounts opened by state, over time

Coverage note. Twenty-nine of the fifty-two ABLE-operating jurisdictions publish AUM figures accessible through Ascensus NAA reports (20 states), Vestwell reports (Alabama, Oregon), and standalone state Treasurer publications (VA, NE, TN, NY, TX, ME, LA, CO, FL, NH). Only nine publish account counts on a regular schedule; the remaining jurisdictions report assets only or do not publish quarterly figures.

Policy briefs

Plain-language briefs translating the research for the three audiences whose decisions determine whether the ABLE enrollment gap closes.

How ABLE protects family savings and benefits

What families of children and adults with disabilities need to know about eligibility, contribution limits, and why an ABLE account does not disqualify SSI or Medicaid.

Read the brief →Why offering ABLE payroll deduction helps your workforce

The business case for adding ABLE contribution as a payroll benefit for employees with disabilities and family members, and how to set it up.

Read the brief →Scaling ABLE enrollment: what the causal evidence supports

The design implications of Yin (2026): where to embed ABLE information, which touchpoints move enrollment, and what the aggregate fiscal response looks like.

Read the brief →Downloads

Dr. Michelle Yin founded REACHABLE to build awareness of the ABLE Act among the eligible population and to promote financial independence for people with disabilities. The consumer platform turns this research into action.

Visit joinreachable.com →