The First Causal Evidence on the ABLE Act

A tool that works, but almost nobody uses.

The Achieving a Better Life Experience Act of 2014 lets people with disabilities save without losing SSI, Medicaid, or other means-tested benefits. The ABLE Age Adjustment Act of 2022, effective January 1, 2026, adds about 6 million newly eligible people, including approximately 1 million veterans.

Enrollment rate: under 3 percent of eligible Americans have an ABLE account, a decade after passage.

Does the policy actually improve financial outcomes for the people it reaches?

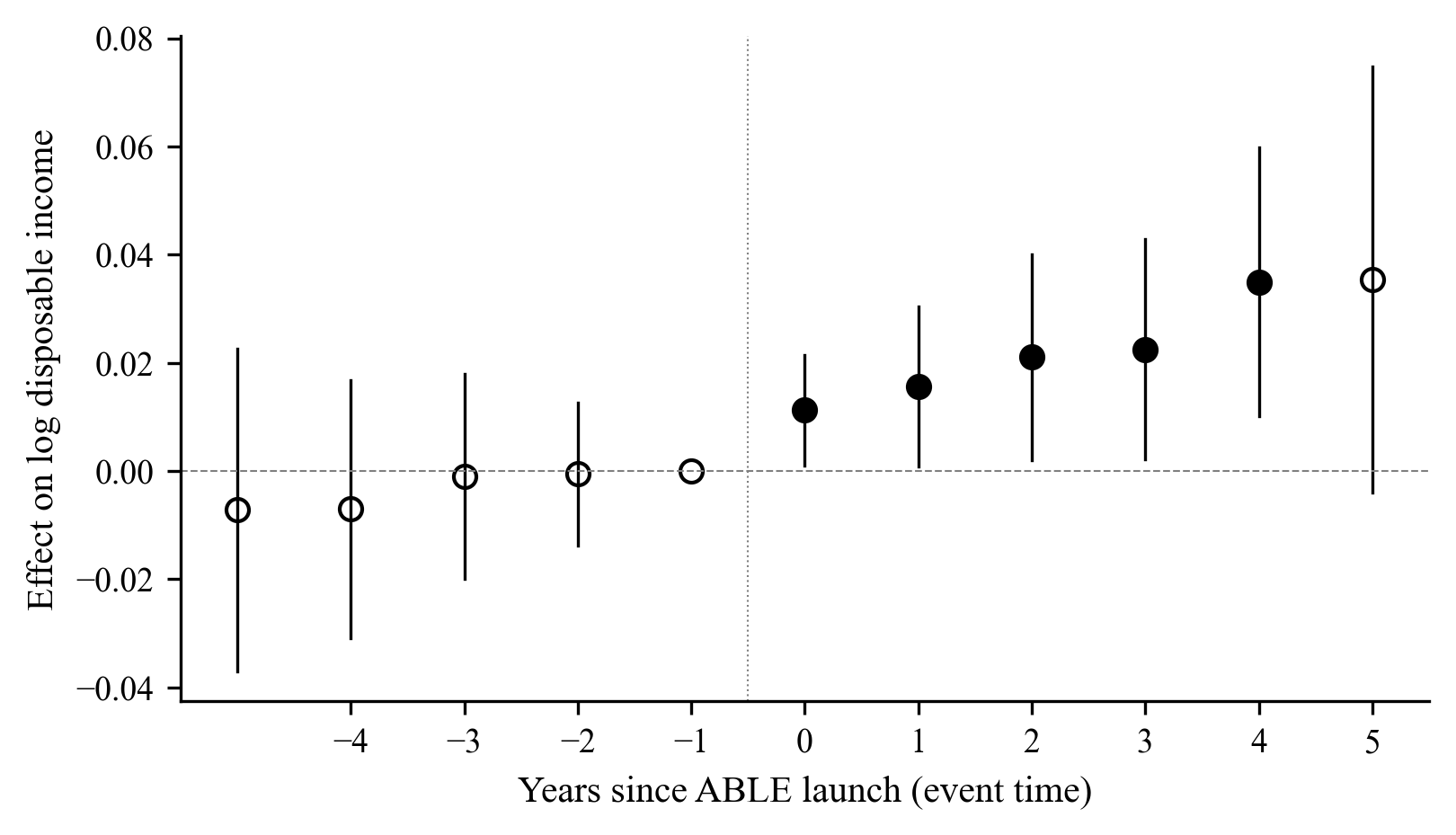

Yin (2026) uses the staggered rollout of state ABLE programs (2016 to 2026) to identify the causal effect of program availability. States that launched their ABLE program in different years form the treatment group. Four states never adopted an ABLE program — North Dakota, South Dakota, Wisconsin, and Nevada — form the control group.

The estimator is Callaway & Sant'Anna's (2021) doubly-robust difference-in-differences, restricted to adults with disabilities. Standard errors clustered at the state level.

ABLE works. When people access it.

ABLE and Medicaid are substitutes.

The ABLE effect is largest in states that did not expand Medicaid under the Affordable Care Act (+3.6 percent disposable income), and approximately zero in states that expanded Medicaid (+0.6 percent, interaction significant at p < 0.10). Both policies relax asset-related constraints on adults with disabilities. Where one is in place, the marginal effect of the other is smaller.

Policy implication. Enrollment outreach in the ten never-expansion states (Alabama, Florida, Georgia, Kansas, Mississippi, South Carolina, Tennessee, Texas, Wisconsin, Wyoming) has the highest per-dollar marginal return on federal outreach investment.

Enrollment is the binding constraint.

The 3 percent enrollment rate binds the population-level impact of a policy that works when accessed. Consumer-facing outreach has been the field's primary tool for a decade. The next decade needs systems integration and trusted-messenger networks to reach the 97 percent.

Embed ABLE inside decision moments

VR intake, SSI application, employer onboarding, IEP transition planning, Medicaid HCBS waiver enrollment. Northwestern's Prong 1 design in the ACL cooperative agreement proposal.

Build trusted-messenger networks

Faith leaders, community health workers, pediatricians, librarians, peer navigators. Two-layer trust structure with peer-navigator hands-on enrollment support at 100,000 sessions by Year 3.

Address benefits-loss misconceptions

The largest single deterrent is the belief that opening an ABLE account triggers SSI or Medicaid ineligibility. It does not. First $100,000 disregarded from SSI; balances up to state limits disregarded from Medicaid.

Prioritize non-expansion states

Given the ABLE-Medicaid substitutability finding, marginal federal outreach dollars deliver the largest financial-inclusion gains in the ten Medicaid non-expansion states.