Asset-Test Relief and the Financial Life of Adults with Disabilities

The Achieving a Better Life Experience (ABLE) Act relaxed the Supplemental Security Income asset test on the asset margin alone, for the first time since the 1996 welfare reforms. Adults with pre-age-26 disability onset can now hold up to $102,000 in an ABLE account without losing SSI, Medicaid, or other means-tested benefits. State programs rolled out in a staggered sequence from 2016 to 2026. This Center brings together the first causal-identification evidence on the ABLE Act, state-year dashboards, and updated 2026 findings on disposable income, wages, employment, and the SSDI-substitution question.

What are you looking for?

Every visitor to this Resource Center has a different question. Pick the card that matches your situation and skip straight to the sections written for you.

I'm an individual or family member.

Learn what ABLE is, who qualifies, how it protects SSI and Medicaid, and where to find free help.

I'm a policymaker or agency lead.

Population effect sizes, take-up gap, Medicaid interaction, and 2026 rollout planning.

I'm an employer or HR partner.

What the $2,000 cliff means for your candidate pool and how to make ABLE visible in benefits.

I'm a researcher or journalist.

Working paper, findings, honest limits on SSDI substitution, and methods.

Pick a path to keep going.

Try the Eligibility Explorer

Answer five short groups of questions. Get personalized results on whether ABLE fits your situation, how it interacts with SSI, SSDI, and Medicaid, and step-by-step application guidance.

Open the Explorer →Learn the basics

The $2,000 asset cliff explained visually. How ABLE interacts with SSI, SSDI, Medicaid, and Medicare.

Continue to Chapter 01 →Get free counseling

Four kinds of free benefit counselors in every state, and five questions to bring to a first appointment.

Chapter 02 →Learn the basics.

Plain-language explainers, animated visuals, and program interactions. Read this chapter if you or someone in your family is on SSI, SSDI, or Medicaid — or if you have never heard of ABLE before.

01.2 How the pieces fit

The $2,000 asset cliff, before and after ABLE.

The Supplemental Security Income asset limit has been $2,000 since 1988. For nearly four decades, an adult on SSI who saved more than that lost the monthly benefit and, in most states, their Medicaid coverage the next month. ABLE lets eligible adults save past the cliff without losing either. The two charts below trace the same person's countable savings over five years — once under the old rules, once with an ABLE account.

Savings hit $2,000. SSI and Medicaid stop.

Under the pre-ABLE rules, any month countable resources exceed $2,000, SSI cash payments end and, in most states, Medicaid ends with them.

ABLE balance grows. Benefits stay intact.

Money held in the ABLE account is invisible to SSI (up to $100K) and to Medicaid (any balance). Countable savings never approach the $2,000 limit. SSDI is unaffected.

ABLE next to SSI, SSDI, and Medicaid.

Four federal programs shape the financial life of most adults with disabilities in the United States. Three of them existed for decades before ABLE. This section shows what each program does, whether it has an asset test, and how ABLE interacts with each — without changing any rule of the other three.

Monthly cash benefit for adults with disabilities who have little income and few assets.

Monthly benefit for workers with a disability who earned enough Social Security credits before disability onset.

Health-insurance coverage for adults with disabilities. In most states, tied to the SSI rule.

Tax-favored savings account for eligible adults with disabilities. Balances don't trigger the SSI or Medicaid asset tests.

What happens to a paycheck: without ABLE.

A single paycheck for an adult with a disability on SSI touches every one of these programs. Without ABLE, saving too much means losing the ones with asset tests.

Paycheck arrives

Wages from a part-time or full-time job.

Save or spend?

Every dollar saved counts toward the $2,000 SSI resource limit.

SSI & Medicaid at risk

Countable savings above $2,000 trigger loss of SSI cash and, in most states, Medicaid.

What happens to a paycheck: with ABLE.

The same paycheck, redirected through an ABLE account, does not push countable savings past the $2,000 limit. Everything else stays in place.

Paycheck arrives

Wages from a part-time or full-time job.

Direct-deposit to ABLE

A portion of each paycheck routes automatically to the ABLE account.

Savings grow, benefits intact

ABLE balance is invisible to SSI (up to $100K) and Medicaid (any size). SSDI is unaffected.

SSDI has no asset test to begin with. ABLE does not change how SSDI eligibility, benefit levels, or the Substantial Gainful Activity earnings ceiling work. If the reader is on SSDI only (not SSI), the ABLE account is still available and useful for saving toward qualified disability expenses, but the "cliff" story does not directly apply. Our July 2026 research does not claim ABLE caused any change in SSDI enrollment at the state level.

Now try the tools built on this material.

Try the Eligibility Explorer

Now that you understand the $2,000 cliff, run your specific situation through the tool. Age, benefits, work, savings, state — personalized in three minutes.

Open the Explorer →Brief for Families

Print-ready RISEI Lab brief. Includes an illustrative "Maria" example walking through what changes with an ABLE account.

Open Brief 01 →ABLE Basics page

Alternative plain-language explainer. Available in English and Spanish. Written with self-advocates and family members.

Read the basics →Get help.

Every state has trained benefit counselors who can walk you through the SSI, SSDI, Medicaid, and ABLE interaction for your specific situation. All of them are free.

02.2 Five questions to ask

Benefit counseling in plain language.

The SSI, SSDI, Medicaid, and ABLE interaction is confusing on purpose. Congress made most of these rules in different decades, for different reasons. A trained benefit counselor can sit with an individual or family for an hour and walk through what happens to their specific check, their specific bank account, and their specific Medicaid card if they open an ABLE account. Every counselor described below is free.

Community Work Incentives Coordinator (CWIC)

Trained by the Social Security Administration under the Work Incentives Planning and Assistance (WIPA) program. Handles the SSI, SSDI, Medicaid, Medicare, and ABLE interaction. Every state has a WIPA project.

Vocational Rehabilitation counselor

Employed by the state's VR agency. Handles employment planning, training, and job placement. Many VR counselors are ABLE-informed and can refer to state ABLE staff or a CWIC.

State ABLE program staff

Employed by the state treasurer's office or its ABLE administrator. Answers questions specific to enrolling, contributing, and using the account. Cannot give benefits advice, but can refer to a CWIC.

Protection & Advocacy for Beneficiaries of Social Security (PABSS)

Legal help when a benefit is denied, terminated, or contested. Every state has a P&A agency, and PABSS specifically handles SSI and SSDI work-related legal issues.

Five questions to ask a benefit counselor.

Bring these to a first appointment. A CWIC or VR counselor can usually answer all five in under an hour once they see the client's award letter.

If I open an ABLE account and my grandmother deposits $5,000 next month, will I lose my SSI check?

No. Gifts deposited into an ABLE account do not count as income to SSI in the month received, and they do not count as a resource. Your monthly SSI check continues as long as your countable resources outside the ABLE account stay under $2,000.

If I take a full-time job, what earnings level would move me off SSI?

SSI phases out gradually as earnings rise. In 2024, roughly $1,971 in monthly earnings would end the SSI cash payment for a single adult with no other income (higher in some states). If your earnings rise into that range, you may qualify for extended Medicaid under Section 1619(b). A CWIC can run the numbers for your state.

I'm on SSDI, not SSI. Does ABLE do anything for me?

SSDI has no asset test to begin with, so ABLE does not "protect" SSDI eligibility the way it protects SSI. But an ABLE account can still be useful for tax-favored saving toward qualified disability expenses. If you're also on Medicare, the interaction is different from Medicaid; a CWIC can explain.

What happens to my ABLE money if I need long-term services and supports later?

You can spend ABLE funds on qualified disability expenses at any time, including personal-care services and assistive technology. If the account holder passes away with a balance, the state Medicaid program can, in some circumstances, seek to recover Medicaid costs from the remaining balance. Some states have opted out of this recovery. A P&A attorney or CWIC can explain your state's policy.

Can my employer contribute to my ABLE account?

Employers can offer payroll-deducted contributions to ABLE the same way they support 401(k) contributions. Employer contributions count toward the annual contribution limit ($18,000 in 2024, plus additional room for working account-holders under the ABLE-to-Work provision).

How to find a benefit counselor in your state.

Every state has a WIPA project. Every state has a VR agency. Every state has a Protection & Advocacy agency. Not every ABLE state has a state program, but Ohio's STABLE accepts residents of any state.

- Find a CWIC. Use the SSA Ticket to Work locator at choosework.ssa.gov/findhelp and search by ZIP code. Or call the Ticket to Work Help Line at 1-866-968-7842.

- Find your state VR agency. The Rehabilitation Services Administration lists every state agency at rsa.ed.gov/about/states.

- Find your state ABLE program. The ABLE National Resource Center at the National Disability Institute maintains a directory at ablenrc.org. It is independent of any single state.

- Find PABSS. Every state has a Protection & Advocacy agency. The National Disability Rights Network maintains a directory at ndrn.org.

- Compare state programs. Use our RISEI state-year dashboard at riseilab.org/able-dashboard-states.html for an independent side-by-side of launch dates, tax deductions, and residency rules.

Bring your own numbers to the appointment.

Try the Eligibility Explorer

Print your Explorer results and bring them to your CWIC session. It gives the counselor a running head start on your specific situation.

Open the Explorer →Compare state ABLE programs

Every state's launch date, tax-deduction status, and Ohio STABLE partnerships in an interactive comparison.

Open the dashboard →Tools & briefs

All three RISEI audience briefs (Families / Policymakers / Employers), the state dashboards, and the eligibility explorer.

Continue to Chapter 03 →Explore the tools.

Interactive state-year dashboards, the plain-language basics page, and audience-specific briefs formatted for print or share. Everything is free to use and share with attribution.

03.2 Audience briefs

Interactive dashboards, evidence, and plain-language guidance

Every visualization on this site is built from public data. Every finding is from a Northwestern working paper with a published preprint. Every plain-language page is co-designed with self-advocates and family members.

State-Year ABLE Launches

Explore when every state launched its ABLE program from 2016 through 2026. Compare state-owned plans, Ohio STABLE partner states, and the four never-adopter states. Filter by launch year, program administrator, or residency rules.

Open state-year dashboard →Causal Evidence Dashboard

Explore the Yin (2026) event-study evidence: log disposable income, transfer share, employment, labor-force participation, and wage income. Five years before and five years after each state launch, with two complementary estimation approaches shown side by side.

Open evidence dashboard →What the Evidence Shows

One-page visual summary of the working paper's main findings: +1.5 to 3.3 percent disposable income, +7.7 percent wage income, +0.67 percentage-point employment, the 43.3 percent quadruple-difference effect among young adults, and the ABLE-Medicaid substitution pattern.

View infographic →ABLE Basics for Individuals & Families

What is an ABLE account? Who qualifies? How do I open one? Does it affect my SSI or Medicaid? Plain-language answers written with self-advocates and family members. Available in English and Spanish.

Read the basics →ABLE Eligibility & Benefit Interaction Explorer

A five-step guided walk-through. Enter your age, current benefits, work situation, savings goals, and state — and get a personalized read on eligibility, interactions with SSI/SSDI/Medicaid, contribution limits that apply to you, and a step-by-step application guide with a documents checklist. No data leaves your browser.

Open the Explorer →ABLE Benefits Impact Calculator

Enter a hypothetical ABLE balance and see what actually happens to SSI, Medicaid, SSDI, food and housing assistance, and other means-tested benefits. Uses SSA POMS SI 01130.740 rules and state-by-state Medicaid ABLE limits. Addresses the most persistent misconception that deters ABLE enrollment.

Open the Calculator →ABLE at Life Transitions

Twelve life-decision moments where ABLE education fits naturally: Part C early intervention, IEP transition planning, vocational rehabilitation intake, SSI or SSDI application, employer benefits onboarding, Medicaid HCBS enrollment, rehabilitation hospital discharge, aging services, assistive technology acquisition, veteran-to-civilian transition, and community re-entry. Each moment carries specific enrollment steps.

Open the Guide →ABLE Myths and Facts

Six most persistent myths about ABLE accounts, and the facts, side by side. SSI loss, Medicaid loss, family contributions, state residency, special-needs trust interaction, and the evidence. Every fact carries a citation to federal rules or peer-reviewed research. Designed to be shared.

Read Myths and Facts →Yin (2026) — Working Paper

ABLE Accounts and the Household Economic Response to Asset-Test Relief. First causal-identification study of the ABLE Act using staggered state rollouts and three complementary data panels (household income, labor market, and Social Security Administration counts).

Read the working paper →RISEI Lab Policy Briefs Nos. 2026-04 to 2026-06

Three RISEI-format policy briefs written for the audiences most likely to act on the evidence. Each brief opens with a plain-language "What This Brief Says" summary, uses an illustrative example, and reads or prints in about five minutes.

See what the research is built on.

The evidence

Preliminary findings from the July 2026 working paper. Illustrative magnitudes, honest limits on the SSDI-substitution question, and plain-language methods.

Continue to Chapter 04 →Brief for Policymakers

Population effect sizes, take-up gap, Medicaid interaction, and 2026 rollout implications. Print-ready RISEI format.

Open Brief 02 →Eligibility Explorer

If you haven't yet, run your own situation through the tool. Personalized results in three minutes.

Open the Explorer →The evidence.

Preliminary findings from the July 2026 working paper. Illustrative magnitudes, an honest note on what the state-year data cannot identify, and a plain-language summary of the empirical approach.

04.2 Honest note on SSDI

04.3 Methods rigor

Asset-test relief appears to move labor supply, wages, and disposable income.

Yin (2026) exploits staggered ABLE launches (2016–2026) across three complementary state-year panels — CPS ASEC disposable income (2008–2023), ACS labor market (2000–2022, 38.3M individual records), and SSA administrative counts (2010–2024). Several modern difference-in-differences approaches designed for staggered rollouts return quantitatively similar paths, so the results do not hinge on any single method. All magnitudes below are illustrative and rounded. The working paper is preliminary; specific coefficients may change.

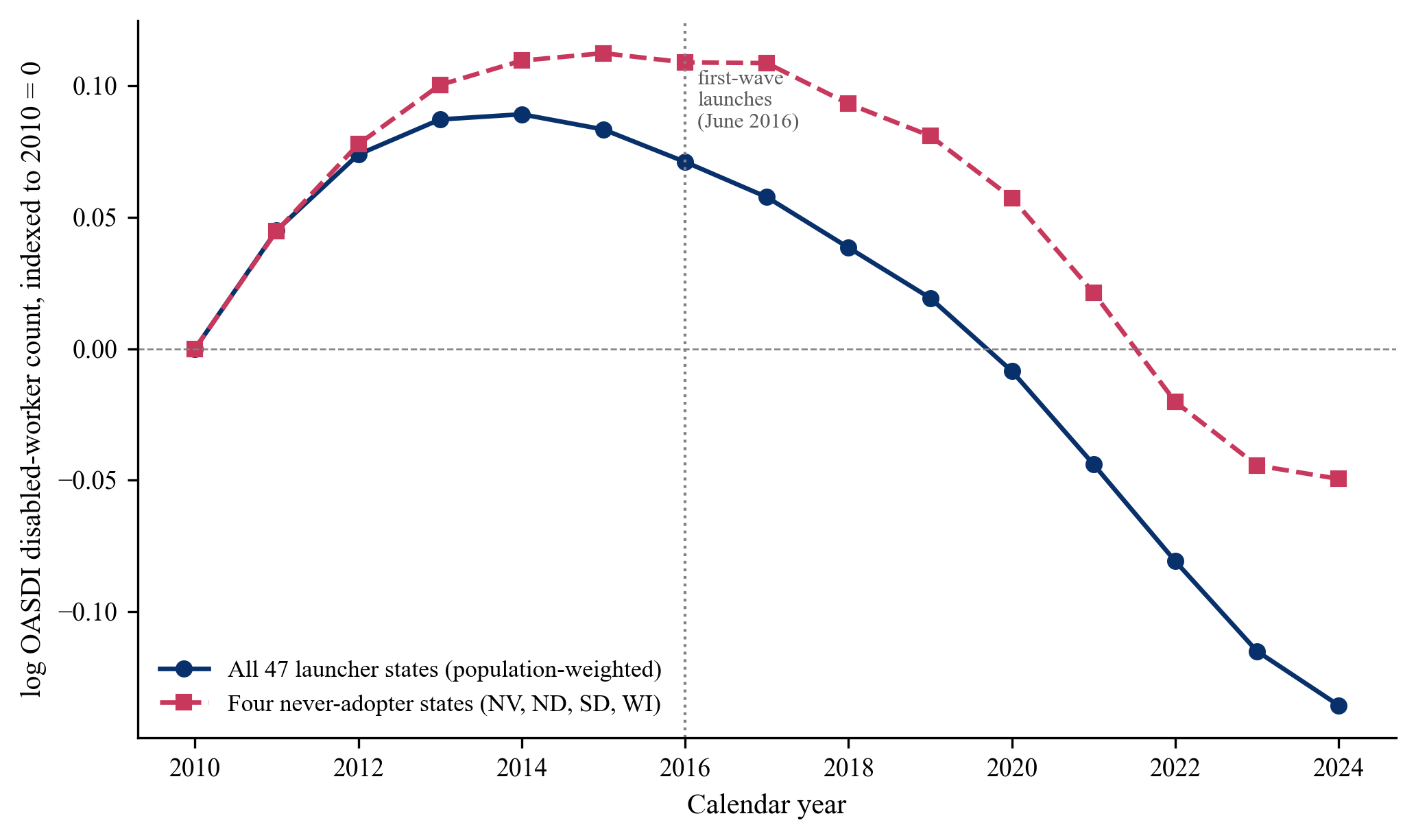

What the state-year evidence can and cannot identify.

A prior version of this Center highlighted a decline in state-year OASDI disabled-worker counts as consistent with ABLE-induced disability-insurance substitution. The July 2026 manuscript updates that reading. State-year SSDI counts did decline after 2015 in launcher states, but they were already declining before ABLE existed, and the four never-adopter states show a nearly identical downward trajectory over the same window. Once state-specific pre-existing trends are absorbed, the estimated effect on SSDI enrollment is not statistically distinguishable from zero. We therefore do not claim ABLE reduced SSDI enrollment. The disposable-income gain operates through higher labor earnings and reduced reliance on cash transfers, not through disability-insurance substitution.

What the design can identify →

The household disposable-income response, the reduction in transfer share, the wage-income response, and the extensive- and intensive-margin labor-supply responses of adults with disabilities. Diagnostics pass on all these outcomes.

What the design cannot identify →

Whether ABLE causally lowered SSDI enrollment. The state-year OASDI decline predates ABLE and continues in never-adopter states. Separating a marginal ABLE contribution from the pre-existing national trend requires individual-level data linked to SSA administrative records.

What comes next →

Individual-level SSA linkage would decompose entry versus exit responses among the eligible population and test the intertemporal saving channel. Data-use agreements with state treasurers, especially Ohio's multi-state STABLE platform, would enable direct measurement of individual account-holder behavior.

Three panels, five estimators, an extensive falsification battery.

The identification strategy triangulates across three state-year panels and five staggered-DiD estimators. Every main coefficient survives placebo tests, cohort splits, alternative control groups, and the cross-border-access attenuation check.

CPS ASEC Disposable Income

2008–2023. Pre-tax personal income minus federal and state income-tax liability computed cell-by-cell with NBER TAXSIM, plus cash transfers. 2,448 state-year-cell observations.

ACS Labor Market

2000–2022, 38.3M individual records aggregated to state-year-disability-age cells. Employment, LFP, log wage income, poverty. Estimation window 2011–2022.

SSA Administrative Counts

2010–2024. OASDI and SSI recipient counts and benefit amounts, aggregated from a 1.006M-observation county-year source panel covering 3,143 counties.

State-and-Year Comparison

Compares outcomes in states that launched ABLE against states that did not, adjusting for state and year differences. Standard errors are clustered at the state, and inference is checked with a bootstrap given the small number of never-adopter states.

Launch-Cohort Event Study

Tracks each state's outcomes five years before and five years after its own launch date, using never-adopter states as the counterfactual. Diagnostics check for pre-existing trends before the launch year.

Robust Alternatives

Two additional modern approaches to staggered-rollout designs reproduce the same event-study path. Results do not hinge on any single method.

Triple & Quadruple Difference

The triple-difference compares adults with and without disabilities within the same state and year. The quadruple-difference adds an age dimension to isolate the pre-age-26 eligibility rule, sharpening identification.

Cross-Border & Placebos

Because Ohio's platform admits residents of any state, some control-state residents can hold accounts and bias the comparison toward zero. Additional specifications and county-border evidence bound the true effect.

Ready to cite the paper?

Cite the working paper

Full citation, abstract, statute references, and contact for the RISEI Lab team. Add to your reference list, media brief, or referee report.

Continue to Chapter 05 →Brief for Policymakers

Population effect sizes, take-up gap, and 2026 rollout. In RISEI Lab brief format. Print-ready.

Open Brief 02 →Evidence dashboard

Explore the event-study path for every outcome and every launch cohort side by side.

Open the dashboard →Cite the paper.

The working paper abstract, canonical citation, statute references, and contact for the RISEI Lab team.

05.2 Working paper & about

The Achieving a Better Life Experience Act of 2014 is the first federal statute since the 1996 welfare reforms to relax an asset test in a major means-tested program, and it does so on the asset margin alone. The disposable-income gain operates through higher labor earnings and reduced reliance on cash transfers rather than through disability-insurance substitution.

Two-page briefs, one page per finding, one PDF per audience.

Each brief is a plain-web page you can read in the browser or print to PDF (Ctrl+P or ⌘+P). Every quantitative claim is cited to Yin (2026), ABLE Accounts and the Household Economic Response to Asset-Test Relief.

ABLE for individuals with disabilities and their families

What ABLE is, who qualifies, how it protects SSI and Medicaid, and what the state-year evidence says about the financial gains. Plain language. Print-ready.

Read · print · shareABLE for state legislators, treasurers, and disability agencies

Population-level effect sizes, take-up gap by state, the Medicaid-expansion interaction, and what the 2026 Age Adjustment Act rollout means for state fiscal projections.

Read · print · shareABLE for employers, HR, and workforce partners

The +7.7% wage-income response, +0.67 pp employment lift, and the 43.3% quadruple-difference wage effect for young adults. Why the asset-test cliff shows up on your hiring pipeline.

Read · print · shareYin (2026) — the July 2026 draft

ABLE Accounts and the Household Economic Response to Asset-Test Relief.

Michelle Yin, Northwestern University · Draft dated July 7, 2026 · Preliminary · JEL codes H31, H55, I18, I38, J14, J22.

Asset tests in means-tested transfer programs impose implicit marginal taxes on saving that can exceed one million percent, yet every prior reform bundled asset-test relief with changes to income limits, benefit levels, or work incentives. The ABLE Act of 2014 relaxes an asset test on the asset margin alone. Exploiting the staggered state rollout across three complementary panels, this paper finds that asset-test relief raises the disposable income of adults with disabilities by 1.5 to 3.3 percent, raises employment by 0.7 percentage points, and raises wage income by 7.7 percent. Effects triple among young adults who satisfy the age-of-onset eligibility rule automatically. The state-year OASDI disabled-worker count declines in launcher states after 2015, but a parallel decline in never-adopter states and pre-2016 differential trends mean the effect on SSDI rolls is not identified once state-specific linear trends are absorbed. Applied to the six million adults newly eligible after January 2026, the estimates imply $1.9 billion in additional annual disposable income.

Why a research-university ABLE Resource Center

The ABLE Resource Center at RISEI Lab is Northwestern's contribution to closing the enrollment gap for a policy that raises disposable income and labor supply for adults with disabilities. We build interactive state-year dashboards from public data, we produce audience-specific briefs with self-advocates and partners, and we generate the causal evidence the field has been missing.

Direction sits with Michelle Yin, Ph.D., Associate Professor of the School of Education and Social Policy at Northwestern, with joint appointments at the Institute for Policy Research (IPR) and the Institute for Public Health and Medicine (IPHAM). All dashboards and briefs on this site are free to use, redistribute, and adapt with attribution.

Cite. Yin, Michelle (2026). ABLE Accounts and the Household Economic Response to Asset-Test Relief. Working paper, RISEI Lab, Northwestern University.

Contact. Michelle Yin: michelle.yin@northwestern.edu · RISEI Lab: risei@northwestern.edu.

Share what you found useful.

Eligibility Explorer

Share this tool with a family member, a client, an HR partner, or a policymaker. It's free, keeps no personal data, and works on any device.

Open the Explorer →Brief for Families

Print-ready RISEI Lab brief. Share with a family member or self-advocate.

Open Brief 01 →Brief for Employers

For HR and workforce partners. Why the $2,000 cliff shows up in the disability-hiring pipeline.

Open Brief 03 →